Overview

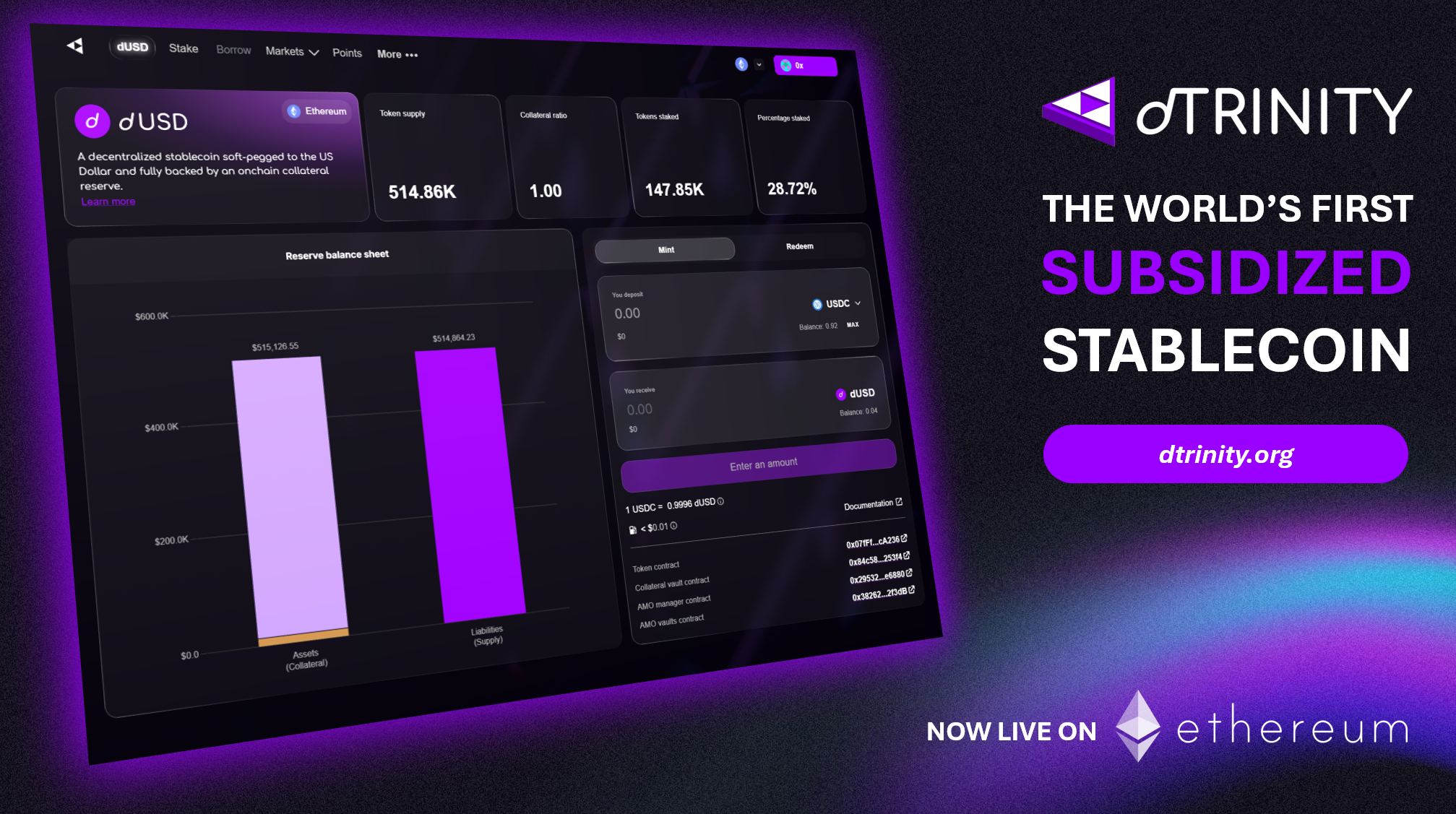

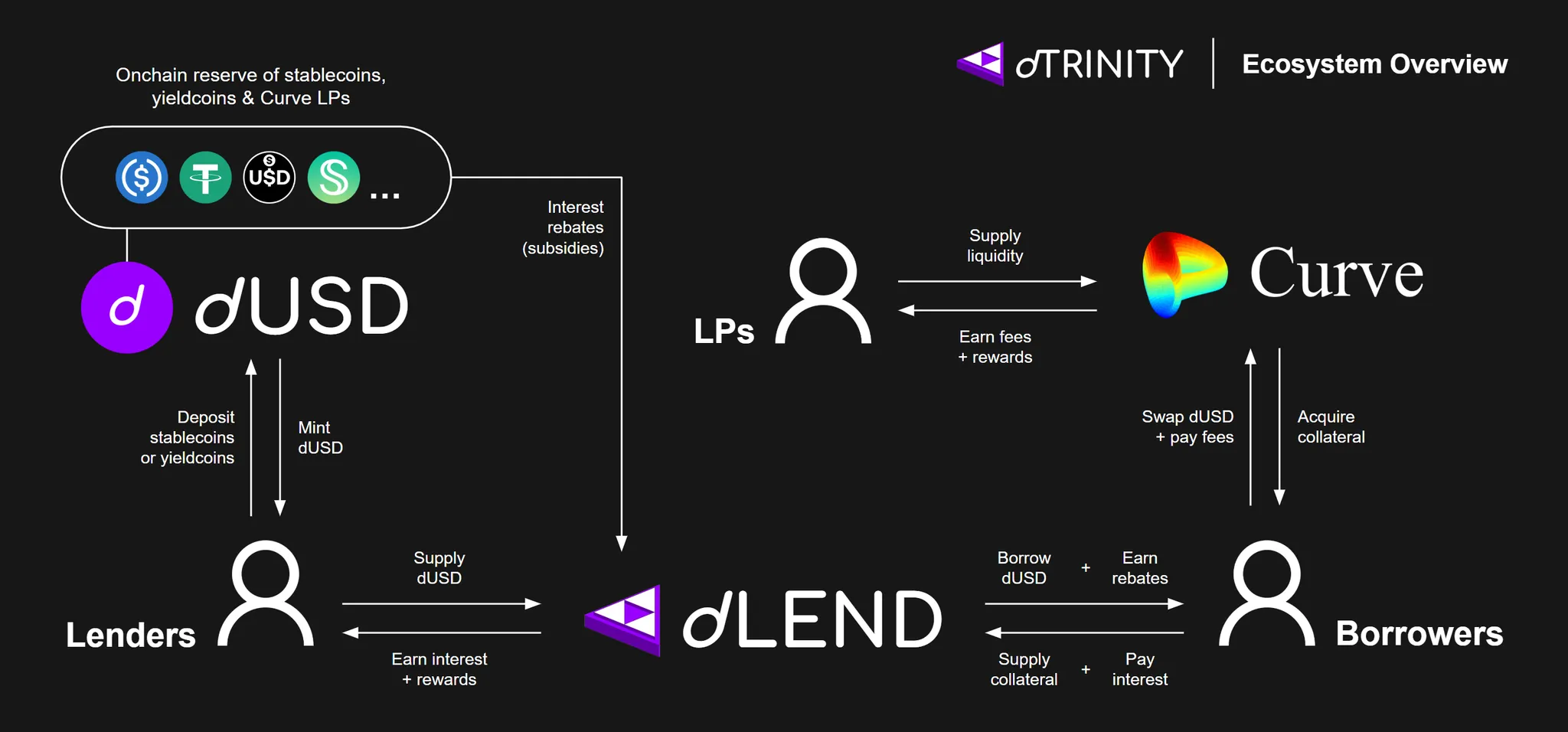

dUSD is a decentralized stablecoin built on the ERC-20 standard. Each token is soft-pegged to the US dollar, backed by at least $1 of collateral held in chain-isolated reserves. Users can mint or redeem dUSD atomically and permissionlessly on a 1:1 basis using eligible reserve assets (minus fees).

Unlike traditional stablecoin models, dUSD’s float revenue can be redirected by the protocol as interest rebates to its borrowers across integrated lending markets, including  dLEND. Additionally, traders and LPs can swap and provide liquidity for dUSD on DEXs such as

dLEND. Additionally, traders and LPs can swap and provide liquidity for dUSD on DEXs such as  Curve.

Curve.

dLEND. Additionally, traders and LPs can swap and provide liquidity for dUSD on DEXs such as Curve.dUSD has no minting fees. Redemptions may incur up to 0.5% in fees.

User Benefits

- dUSD borrowers benefit from lower net interest rates and improved capital efficiency. Yield loopers who borrow dUSD also benefit from subsidized leverage, which may increase carry potential.

- dUSD lenders, including stakers (

sdUSD holders), benefit from structurally higher utilization and yields, driven by subsidized credit demand.

- dUSD and sdUSD LPs benefit from increased trading volume and fee generation, boosted by subsidy-driven money velocity.

For user instructions and current opportunities, please refer to the User Guide.

Chain-Isolated Reserves

dUSD is deployed natively on Ethereum, Fraxtal, and Katana. Each network deployment maintains fully isolated reserves to mitigate chain-specific contagion risk. As a result, dUSD tokens may share the same name across networks, but they are not fungible across chains (e.g., Ethereum dUSD ≠ Fraxtal dUSD).

Below are dUSD addresses on each supported network:

Name | Token Contract | Collateral Vault (Idle Reserve) | AMO Manager | AMO Vault (Deployed Reserve) |

Ethereum dUSD | ||||

Fraxtal dUSD | ||||

Katana dUSD | N/A |

For more information, please refer to  Network Support and Addresses.

Network Support and Addresses.

Network Support and Addresses.Reserve Assets

dUSD's underlying reserves may consist of stablecoins, yieldcoins, and Curve LP positions, providing at least 100% backing for the circulating supply.

Each reserve asset is strategically selected based on its track record, quality, risk profile, and network availability. Protocol governance may add, remove, or adjust exposure to reserve assets over time in response to market conditions and ongoing risk assessments. If the reserve becomes under-collateralized on any network, governance may temporarily pause dUSD minting/redemption and incentives on that network to protect existing users and support re-collateralization.

At the moment, only assets from the following established issuers and protocols may be accepted into the reserves, subject to network availability:

Ethereum | Fraxtal | Katana | |

Tether | ✔️ | ✔️ | ❌ |

Circle | ✔️ | ✔️ | ❌ |

Sky (fka MakerDAO) | ✔️ | ✔️ | ❌ |

Frax Finance | ✔️ | ✔️ | ✔️ |

Curve Finance | ✔️ | ✔️ | ❌ |

Agora Finance | ❌ | ❌ | ✔️ |

Vault Bridge | ❌ | ❌ | ✔️ |

The following assets are currently accepted as reserve assets:

Ethereum

Asset | Status | Mint | Redeem | Type | Issuer | Deployment |

USDC | ✔️ | ✔️ | ✔️ | Stablecoin | Circle | Native |

USDT | ✔️ | ✔️ | ✔️ | Stablecoin | Tether | Native |

USDS | ✔️ | ✔️ | ✔️ | Stablecoin | Sky | Native |

sUSDS | ✔️ | ✔️ | ✔️ | Yieldcoin | Sky | Native |

frxUSD | ✔️ | ✔️ | ✔️ | Stablecoin | Frax Finance | Native |

sfrxUSD | ✔️ | ✔️ | ✔️ | Yieldcoin | Frax Finance | Native |

dUSD/sfrxUSD Curve LP | ✔️ | ❌ | ❌ | LP receipt | Curve Finance | Native |

dUSD/sUSDS Curve LP | ✔️ | ❌ | ❌ | LP receipt | Curve Finance | Native |

Fraxtal

Asset | Status | Mint | Redeem | Type | Issuer | Deployment |

USDC | ✔️ | ✔️ | ✔️ | Stablecoin | Circle | Bridged |

USDT | ✔️ | ✔️ | ✔️ | Stablecoin | Tether | Bridged |

DAI | ✔️ | ✔️ | ✔️ | Stablecoin | Sky | Bridged |

sDAI | ✔️ | ✔️ | ✔️ | Yieldcoin | Sky | Bridged |

frxUSD | ✔️ | ✔️ | ✔️ | Stablecoin | Frax Finance | Native |

sfrxUSD | ✔️ | ✔️ | ✔️ | Yieldcoin | Frax Finance | Native |

dUSD/sfrxUSD Curve LP | ✔️ | ❌ | ❌ | LP staking receipt | Curve Finance | Native |

Bridged assets on Fraxtal are issued by its native bridge, backed by the same underlying collateral on Ethereum.

Katana

Asset | Status | Mint | Redeem | Type | Issuer | Deployment |

vbUSDC | ✔️ | ✔️ | ✔️ | Stablecoin | Vault Bridge | Native |

vbUSDT | ✔️ | ✔️ | ✔️ | Stablecoin | Vault Bridge | Native |

AUSD | ✔️ | ✔️ | ✔️ | Stablecoin | Agora Finance | Native |

frxUSD | ✔️ | ✔️ | ✔️ | Stablecoin | Frax Finance | Native |

sfrxUSD | ✔️ | ✔️ | ✔️ | Yieldcoin | Frax Finance | Native |

vbUSDT and vbUSDT are Katana-native stablecoins issued via the AggLayer bridge, backed by lending vaults on Ethereum. Since the underlying collateral is rehypothecated, Vault Bridge tokens are not considered bridged assets.

Price Oracles

dUSD’s reserve NAV (net asset value) and reserve asset minting/redemption ratios are determined by price feeds via third-party oracle providers like Api3 and Chainlink, as well as direct feeds from the asset’s issuer. Additional oracle providers may be integrated over time to improve redundancy and reliability.

Oracle Methodology

- For minting, redeeming, lending, and borrowing transactions, dUSD’s price is hard-coded at $1 to prevent potential market manipulation. Since dUSD is disabled as a collateral to secure loans across integrated markets by default, hard-coding its price minimizes oracle-related risk without impacting lending operations.

- If a stablecoin’s market feed reports a price anomaly above $1, dUSD’s oracle integration will round it down to exactly $1, preventing minting activity from posing under-collateralization risk.

- To enhance pricing accuracy, oracles for yieldcoins and Curve LP positions rely on composite feeds to calculate the underlying value rather than exchange-traded prices alone, mitigating potential risk from market liquidity issues.

Examples

For more information, please refer to Oracle Integrations.

Stability Mechanisms

1. Atomic Minting & Redemption

The ability to mint and redeem dUSD 1:1 against its underlying reserves enables a primary market hard peg and a secondary market soft peg for the token.

When dUSD trades at a discount vs. $1, arbitrageurs can mint dUSD at par (hard peg) and sell it on the open market, increasing circulating supply while pushing the price back down (soft peg). Conversely, when dUSD trades at a premium vs. $1, arbitrageurs can buy discounted dUSD and redeem it at par (hard peg), contracting supply while pushing the price back up (soft peg). This natural process is how most stablecoins maintain their peg stability.

dUSD's redemption fee also influences where arbitrageurs are incentivized to step in, which affects how far below $1 the token may trade. For example, a 0.5% redemption fee means dUSD may trade around $0.995, where further deviations would be arbitraged away by market participants and/or SMOs.

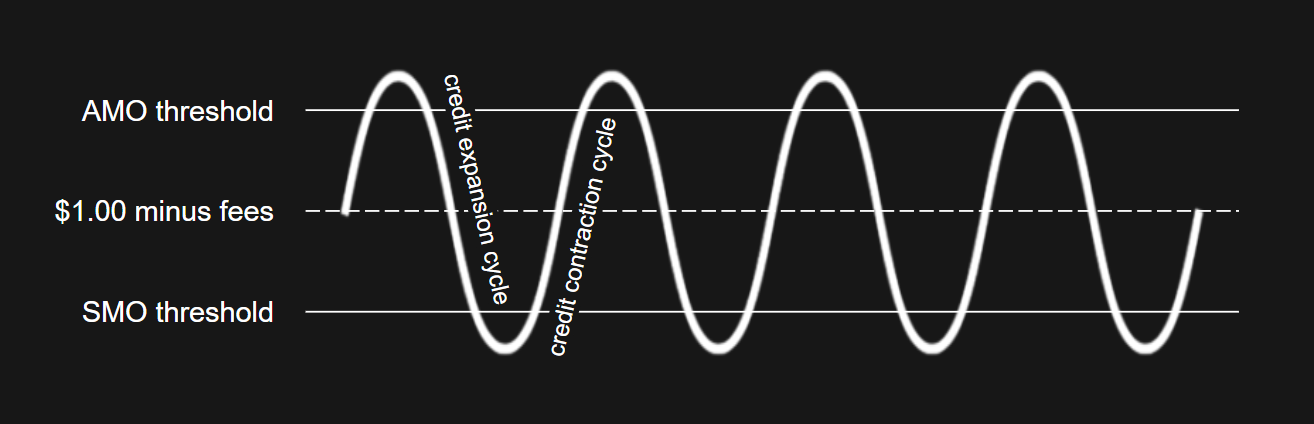

2. Stability Market Operation (SMO)

SMOs are akin to the Fed selling assets on the open market to reduce its balance sheet and the fiat money supply. Similarly, dTRINITY’s SMOs contract circulating supply by selling reserves on DEXs to buy back and burn dUSD. When dUSD trades at a discount, SMOs help restore peg stability and capture potential arbitrage revenue for the protocol.

SMO are strategically executed to defend dUSD’s peg in the event of low market arbitrage activity. These operations typically take place during credit expansion cycles when there is more selling pressure from dUSD borrowers.

3. Algorithmic Market Operation (AMO)

AMOs are akin to the Fed buying assets on the open market to expand its balance sheet and the fiat money supply. Similarly, dTRINITY’s AMOs can grow dUSD’s circulating supply by creating new tokens to deploy into DEX liquidity pools alongside paired reserve assets. When dUSD trades at a premium, AMOs help restore peg stability and capture potential arbitrage revenue for the protocol.

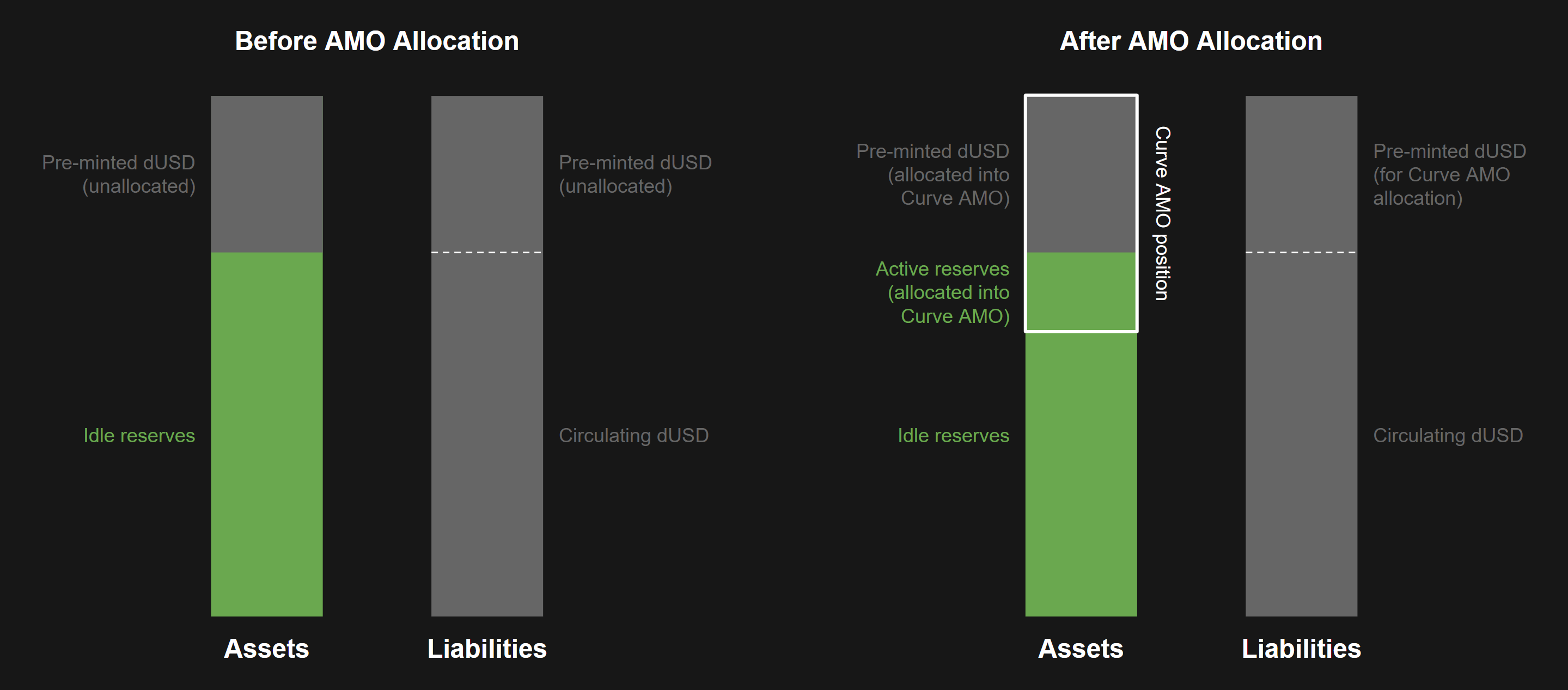

Also known as “direct deposit modules,” AMOs were originally pioneered by Frax Finance in 2021. They enable onchain market operations where stablecoins are pre-minted and deployed into DEXs alongside paired reserve assets to provide liquidity without significantly impacting peg stability.

Pre-minted stablecoins in AMOs are backed by protocol-owned LP positions. Once swapped out of the AMO, these tokens become collateralized by assets that are simultaneously swapped into the AMO. Collateralized tokens can also be swapped back into the AMO in exchange for deployed reserve assets, returning them to the pre-minted state.

AMOs for dUSD are deployed on Curve Finance across supported networks. Curve is currently dTRINITY’s only AMO venue due to its established track record, efficient StableSwap AMM (automated market maker), and mature security profile for protocol-owned liquidity.

Curve AMOs enable dTRINITY to enhance peg stability, capital efficiency, and protocol revenue, unlocking greater liquidity and incentive funding for its users.

- Peg stability can be enhanced through AMOs by injecting pre-minted dUSD into Curve pools to reduce price premiums when paired-asset liquidity is high, or by reabsorbing dUSD from Curve pools to narrow price discounts when paired-asset liquidity is low.

- Capital efficiency can be improved by leveraging existing reserves plus pre-minted dUSD to bootstrap TVL and secondary market liquidity. Similar to LPs, AMO deployments may earn trading fees and reward emissions from Curve. Protocol-owned liquidity in AMO pools may amplify these earnings, further boosting reserve productivity.

- Protocol revenue may increase through a combination of AMO yield farming and arbitrage profits, providing additional funding for user incentives or building excess reserves. However, AMO earnings may fluctuate based on market conditions. When they are not profitable, the protocol may reduce AMO activity until market conditions improve.

4. Excess Reserves

Over time, a portion of float revenue and AMO net earnings may accumulate as excess reserves, pushing dUSD’s reserve ratio above 100%. This helps further strengthen market confidence and dUSD’s peg stability while gradually building up a risk buffer. When the reserve ratio exceeds a certain threshold, protocol governance may determine how to allocate the excess reserves.

Adaptive Incentives

dTRINITY allocates most of its reserves into productive assets and AMO positions. These holdings are optimized to target DeFi yield benchmarks (e.g., Aave USDC), allowing the protocol to generate competitive earnings. New dUSD is minted periodically by the protocol against the majority of net earnings accrued during that period to fund user incentives across the market.

Adaptive incentives refer to dTRINITY’s ability to optimize incentive allocations among borrowers, lenders, and/or LPs. Incentives can be directed to the demand side (borrowers), the supply side (lenders and LPs), or both, subject to market conditions and protocol governance.

- When credit demand weakens, a greater share of incentives can be directed toward borrowers to stimulate utilization and debt expansion.

- Conversely, when supply inflows are lagging, incentives can be shifted toward lenders and LPs to attract new reserves, lending deposits, and liquidity, providing fuel for further expansion.

Incentive Optimization

Supply-side incentives can be optimized by routing them toward sdUSD liquidity pools on Curve rather than to dUSD lenders directly, since sdUSD holders and LPs are effectively dUSD lenders. Depending on market conditions, dTRINITY may leverage Curve’s veTokenomics to amplify its incentives through CRV emissions.

Incentivizing sdUSD pools enables LPs to earn both trading fees and CRV emissions on top of lending yield, enhancing their overall performance and capital efficiency. Not only does this help expand reserves and credit supply for the protocol, it also reinforces market liquidity and peg stability via cross-pool arbitrage between dUSD and sdUSD.

Reserve Expansion | Credit Supply Expansion | Debt Expansion | Liquidity Expansion | |

dUSD Borrower Rebates | ❌ | ❌ | ✔️ | ❌ |

dUSD Lender Rewards | ✔️ | ✔️ | ❌ | ❌ |

dUSD LP Rewards | ✔️ | ❌ | ❌ | ✔️ |

sdUSD LP Rewards | ✔️ | ✔️ | ❌ | ✔️ |

Incentive Distribution Venues

The following platforms are currently whitelisted for incentive distribution. Additional venues may be included in the future based on protocol governance and strategic partnership opportunities.

dTRINITY also partners with Merkl to support venues that do not have a native system to intake external incentives.

Lending Protocols

dUSD Borrower Rebate | dUSD Lender Reward | |

dLEND

(Ethereum, Fraxtal) | ✔️ | ✔️ |

Morpho

(Katana) | ✔️ | ❌ |

DEXs

dUSD LP

Reward | sdUSD LP

Reward | |

Curve

(Ethereum, Fraxtal) | ✔️ | ✔️ |

Sushi Swap

(Katana) | ✔️ | ❌ |

Incentive Methodology

Below is how incentives are calculated for different types of market participants. In addition to float revenue (including AMO net earnings), dTRINITY may allocate other sources of revenue and growth budgets toward funding user incentives, subject to market conditions and protocol governance.

Description | Significance | |

Debt-to-Reserve Ratio

(Debt Ratio) | Aggregate Debt / (M0 - dUSD in AMOs) | dUSD debt expansion relative to its organic reserve base. This ratio helps determine how much float revenue can be distributed as borrower rebates per unit of debt. |

Lending-to-Reserve Ratio

(Lending Ratio) | Aggregate Lending TVL / (M0 - dUSD in AMOs) | dUSD credit supply relative to its organic reserve base. This ratio helps determine how much float revenue can be distributed as lender rewards per unit of TVL.

Note: dTRINITY rebates borrowers by default. Some float revenue may be shared with lenders as rewards, depending on market conditions. |

Liquidity-to-Reserve Ratio

(Liquidity Ratio) | Aggregate Liquidity TVL / (M0 - dUSD in AMOs) | dUSD + sdUSD secondary market liquidity relative to the organic reserve base. This ratio helps determine how much float revenue can be distributed as LP rewards per unit of TVL.

Note: Some float revenue may also be shared with LPs as rewards, depending on market conditions. |

Float APY | (Float Revenue - Retained Float Revenue) / (M0 - dUSD in AMOs) | Exogenous yield (float revenue) generated from reserves provides the core source of funding for dUSD user incentives, minus any protocol retentions. |

Borrower Rebate APY | (Float APY / Debt Ratio) × Market Weight | Variable interest rebate rate for dUSD borrowers per market by weight, reducing their net cost per unit of debt. |

Lender Reward APY | (Float APY / Lending Ratio) × Market Weight | Variable supply reward rate for dUSD lenders per market by weight, enhancing their net yield per unit of TVL. |

LP Reward APY | (Float APY / Liquidity Ratio) × Market Weight | Variable supply reward rate for dUSD and/or sdUSD LPs per market by weight, enhancing their net yield per unit of TVL. |

For more details, please refer to 📊 Stablecoinomics.