Overview

dLEND is dTRINITY’s native lending protocol, forked from Aave v3. It is powered subsidized markets for dSTABLE assets like  dUSD,

dUSD,  dS,

dS,  dETH, and

dETH, and  dBTC. On top of the existing v3 features and mechanics which can be referenced through Aave’s documentation, dLEND incorporates several unique features that enable lower credit costs and better yields for protocol users.

dBTC. On top of the existing v3 features and mechanics which can be referenced through Aave’s documentation, dLEND incorporates several unique features that enable lower credit costs and better yields for protocol users.

dUSD, dS, dETH, and dBTC. On top of the existing v3 features and mechanics which can be referenced through Aave’s documentation, dLEND incorporates several unique features that enable lower credit costs and better yields for protocol users.dSTABLE Markets

dSTABLE money markets are the credit engine of the dTRINITY ecosystem. Lenders who supply tokens in dSTABLE markets on dLEND can earn yields and rewards from ecosystem partners and/or the protocol. Borrowers can then supply multiple collateral assets to borrow dSTABLE tokens and earn interest rebates as well as intrinsic yields/points from their collateral (as applicable).

dLEND enhances user experience by consolidating lending and borrowing into dSTABLE assets. Borrowers benefit from exogenous interest rebates, which lower net borrowing costs below market rates—making dLEND an ideal platform for leverage and yield-looping strategies. These subsidies also drive sustained credit demand, pushing utilization to consistently high levels. As a result, dSTABLE Supply APYs on dLEND may rise above market rates, delivering superior yields to lenders and reducing their opportunity costs.

Most importantly, subsidized borrowers don’t need to employ as much leverage to achieve a similar return profile compared to using unsubsidized stablecoins. This reduces risk while still maintaining attractive yields, making leverage/looping strategies more capital-efficient and resilient on dLEND.

User Incentives

Supply dSTABLE | Borrow dSTABLE | |

☑️ | N/A | |

Main Yield Source | Supply APY (from lending) | Intrinsic APY (from yield-bearing collateral) |

Other Yield Sources | Reward APY (from ecosystem partners) | Rebate APY (from dSTABLE subsidies) |

Other Incentives | Third-party points (from ecosystem partners) | Third-party points (from ecosystem partners) |

For a complete list of markets and incentives, please refer to Yields & Rewards.

Key Parameters

- dSTABLE assets are the only tokens enabled for borrowing on dLEND by default. Therefore, only dSTABLE markets have lending/borrowing rates.

- Collateral rehypothecation on dLEND is disabled by default to mitigate nested leverage and liquidation risks during volatile markets. However, collateral deposits with intrinsic yields may still appreciate within dLEND.

- dSTABLE assets are disabled as collateral for borrowing to prevent subsidy arbitrage from users who may loop a dSTABLE asset against itself.

- The Max LTV (loan to value) ratio to borrow varies by collateral but may not exceed 80% in order to limit liquidation risk. This implies a maximum leverage capacity of 5x on dLEND (at 80% LTV).

- Liquidation LTV = Max LTV of collateral + 5 percentage points (as high as 85% LLTV).

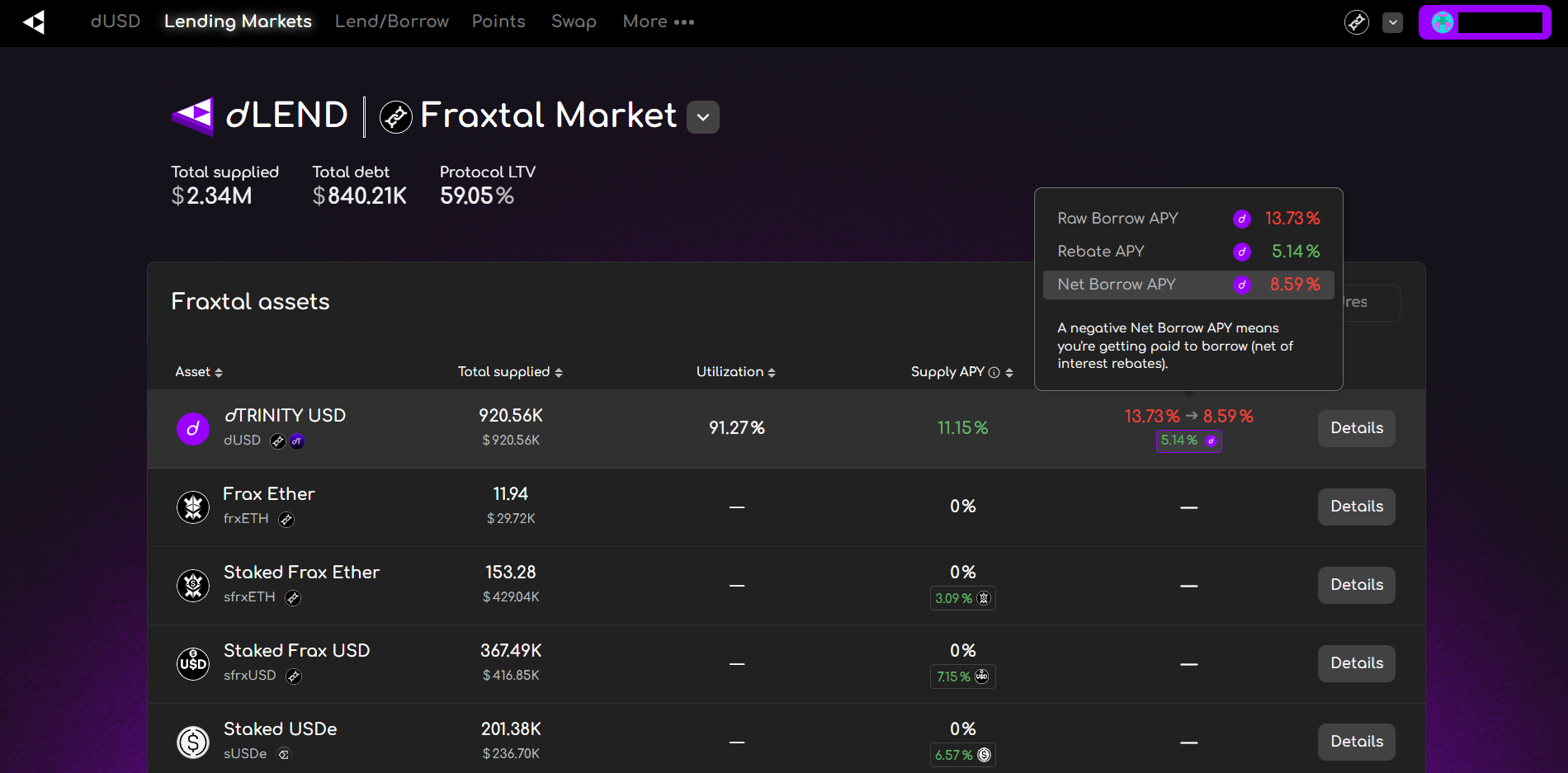

Dynamic Interest Rate Model

dLEND utilizes the standard dynamic interest rate model forked from Aave. Like Aave, Supply and Borrow APYs adjust in real time based on the utilization ratio of each market. However, dLEND introduces a key innovation: dSTABLE borrowing subsidies (interest rebates). These rebates are distributed proportionally to outstanding dSTABLE debt, effectively lowering the net Borrow APY. As a result, the dLEND rate curve behaves differently—especially at lower utilization levels.

When utilization is low, there is less total debt competing for available subsidies, causing the effective Borrow APY to decline steeply, even becoming negative. In such cases, users may get paid to borrow, net of rebates. This dynamic creates a powerful incentive to borrow whenever the market is underutilized, effectively guaranteeing high utilization over time—since leaving “free money” on the table is unlikely in an efficient market environment.

Price Oracles

dLEND utilizes external oracles like Api3, RedStone, and Chainlink to value collateral deposits and manage liquidations. More oracles will be incorporated in the future to enhance the reliability of price feeds.

To protect against de-pegging events caused by temporary market liquidity issues, oracle price feeds for LSTs and yieldcoins are based on the unit NAV of their underlying holdings rather than market-traded prices. For example, Api3 provides a feed for sfrxUSD/frxUSD (how much frxUSD is staked per sfrxUSD) and frxUSD/USD (how much frxUSD is trading for). The final price of sfrxUSD is then determined by multiplying sfrxUSD/frxUSD with frxUSD/USD.

Additionally, the price of dSTABLE assets are hardcoded on dLEND as follows:

dUSD | dS | dETH | dBTC |

1 dUSD = 1 USD | 1 dS = 1 S | 1 dETH = 1 ETH | 1 dBTC = 1 BTC |

Since dSTABLE assets are disabled as borrowing collateral, hardcoding their prices has no impact on liquidations. Hardcoding also prevents borrowing capacity manipulation on dLEND when a dSTABLE asset trades above par. At the same time, borrowers can repay their loans at face value on dLEND—especially when dSTABLE assets trade below par—thereby incentivizing natural arbitrage from borrowers to deleverage and restore price stability.

Liquidation

Borrowers can be liquidated if their LTV ratio exceeds the predefined Liquidation LTV, which varies by collateral. This is tracked via the borrower’s Health Factor, where a value of less than 1.00 would start triggering liquidation. dLEND’s liquidation mechanism is similar to Aave’s, where up to a specific percentage (typically 50%–75%, depending on the asset) of a borrower's collateral may be seized and sold to repay part of the debt once the Liquidation LTV is breached.

Like on Aave, liquidations on dLEND are permissionless and can be executed by any market participant. Liquidators repay a portion of the borrower's outstanding debt and, in return, receive a discounted portion of the collateral. The liquidation bonus and protocol fee vary by market and asset, and are designed to ensure strong economic incentives for maintaining solvency. Notably, liquidators can utilize dSTABLE flash loans to to execute liquidations without upfront capital—further enhancing efficiency and responsiveness in volatile market conditions.

To avoid liquidation, borrowers can:

- Deposit additional collateral to increase their Health Factor

- Partially or fully repay their outstanding debt